Kamagra gibt es auch als Kautabletten, die sich schneller auflösen als normale Pillen. Manche Patienten empfinden das als angenehmer. Wer sich informieren will, findet Hinweise unter kamagra kautabletten.

Aec report

Pre-Feasibility of a Central

Queensland Intermodal Logistics

Final Report – Baseline Analysis

and Pre-Feasibility Assessment

Central Queensland Intermodal

Logistics Hub Incorporated

Final Report

July, 2012

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Document Control

Pre-Feasibility of a Central Queensland Intermodal Logistics Hub

Central Queensland Intermodal Logistics Hub Inc

Michael Campbell

CQILH Logistics Hub Feasibility - Pre-Feasibility and Baseline Analysis

Final Report 1.0

11/7/2012 11:34 AM

Reviewed

Approved

Final Report v1.0

Whilst all care and diligence have been exercised in the preparation of this report, AEC Group Limited does not

warrant the accuracy of the information contained within and accepts no liability for any loss or damage that

may be suffered as a result of reliance on this information, whether or not there has been any error, omission

or negligence on the part of AEC Group Limited or their employees. Any forecasts or projections used in the

analysis can be affected by a number of unforeseen variables, and as such no warranty is given that a

particular set of results will in fact be achieved.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Executive Summary

Background

Central Queensland is experiencing a period of economic and population growth closely linked to its abundant natural resources. The transport industry has a critical role in enabling ongoing development and the potential opportunity to establish an intermodal logistics hub in Central Queensland has been discussed for several years.

Developing a logistics hub in Central Queensland may be viable, given its proximity to three major natural resource areas, the well established agricultural sector and its ability to service areas to the north, south and west. However, the initial capital investment required is significant.

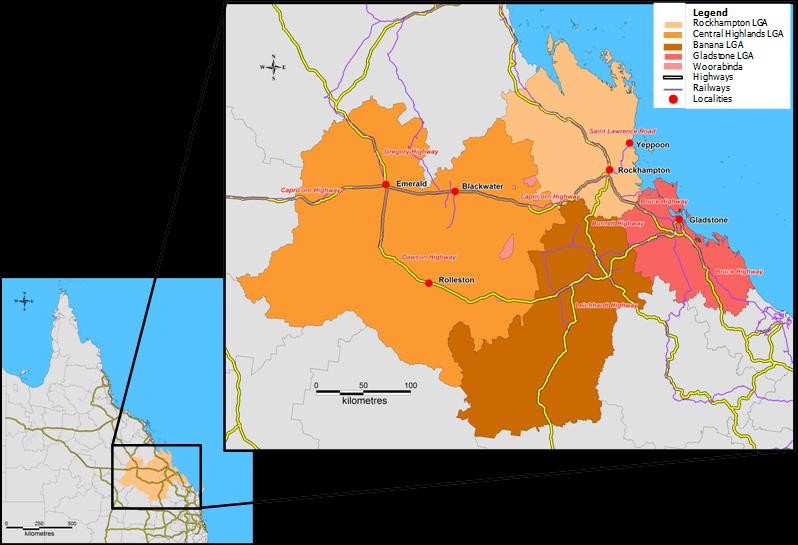

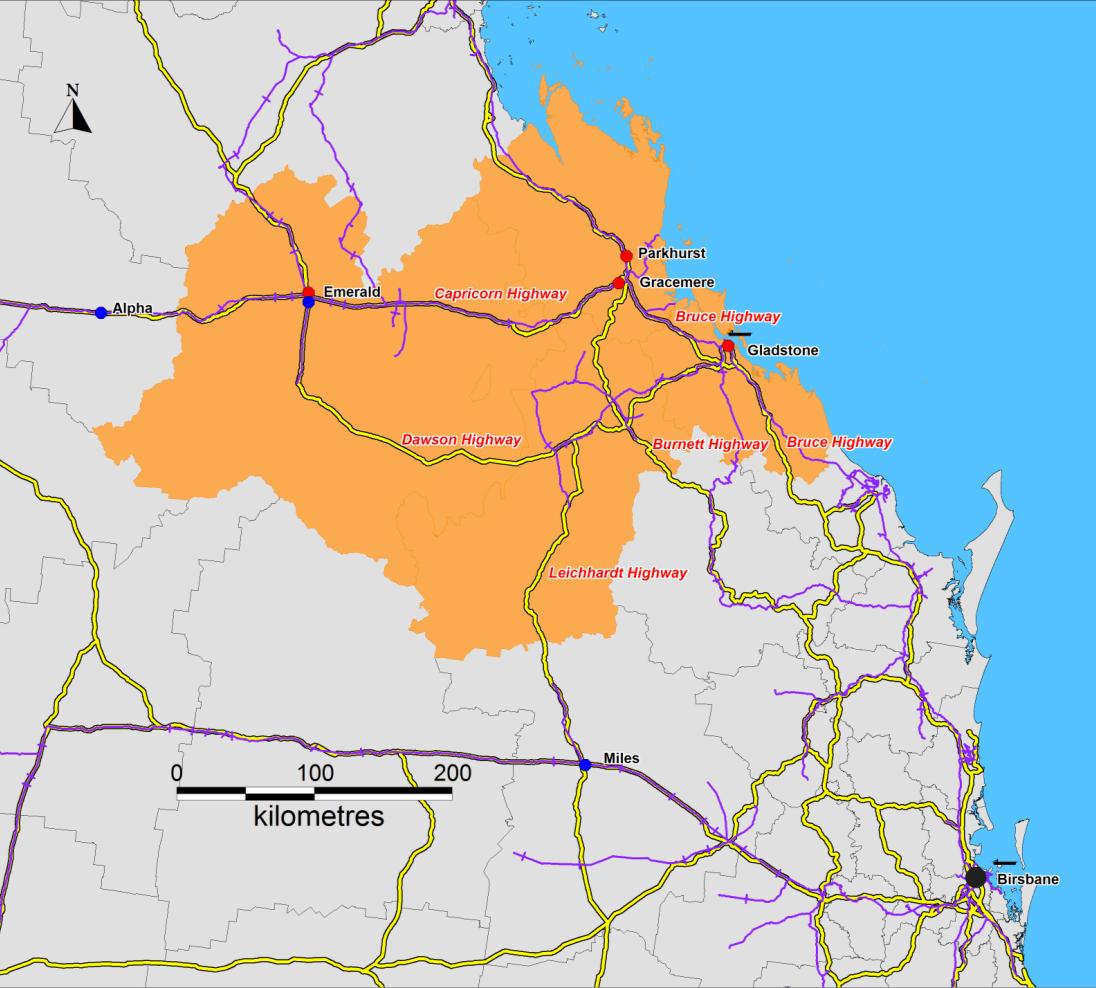

The following map introduces the local government areas (LGAs) that make up the catchment for the study - the Fitzroy Statistical Division (SD).

Figure ES.1. Local Government Areas in Fitzroy SD

Source: AECgroup

An intermodal hub would provide a critical piece of regional transport infrastructure, increase efficiency in the sector and help ensure the regional economy is not constrained by high transport costs. However, the development will only proceed where there is sufficient demand to make the facility commercially viable.

Queensland has one of the fastest growing economies in Australia, unpinned by growth in the mining and energy sectors. Workers are moving from interstate and overseas to take up jobs. Population growth is strong and expected to continue, with an additional 2.5 million people forecast to live in Queensland by 2031 (DLGP, 2011c).

A major challenge for the Queensland Government is to actively manage the impacts of this growth. By investing in infrastructure and services to support growth in regional

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

areas, people will be encouraged to settle outside of South East Queensland. Attracting workers to regional Queensland, where and when they are needed, is an essential part of the government's population growth strategy. The following figure illustrates the anticipated population size and growth rate in the catchment to 2031.

Figure ES.2. Forecast Population Growth, Fitzroy SD

Fitzroy SD Population

Fitzroy SD Populatin Growth Rate

QLD Population Growth Rate

Source: ABS (2011a), Queensland Treasury (2011), DIP (2008).

Currently, the mining and energy industries are strong drivers of population growth and investment. The region is rich in high quality coking coal, much of which is exported through the Port of Gladstone. Central Queensland also produces a significant amount of the state's electricity from the Stanwell, Gladstone and Callide power stations (DEEDI, 2011). The infrastructure requirements to meet the growing needs of the region are substantial. Significant public and private sector investment is already occurring in the region (e.g. Port of Gladstone expansions). There is increasing pressure on transport infrastructure, community resources and utilities to meet industry demands.

Despite ongoing concerns over the global economic outlook, industry stakeholders remain confident of continued growth of the resources sector in the region, including forecasts of new developments and increased capacity. This is supported by state government forecasts that by 2030 the Queensland production of coal is expected to peak at approximately 340 million tonnes annually, equating to production increasing by approximately 5.5% per annum (Department of Infrastructure and Planning, 2010).

Primary industries are economically important in Central Queensland. Grazing is a major industry with Rockhampton promoting itself as Australia's beef capital. Further, grain production within Central Queensland is forecast to remain relatively stable over the coming years, in line with the ABARES (2011) estimates for Australia. The main factor for grain production which will affect the Fitzroy SD's GRP will come as a result of increases in the price for grain due to increased global demand.

Pre-Feasibility Assessment

The pre-feasibility assessment is based on a comparison of lease rates necessary to recover a developer's capital costs compared to market expectations. Market expectations were determined through a broad stakeholder consultation exercise with reference to recent sales of industrial land. The pre-feasibility assessment is not intended to provide a full feasibility assessment of each opportunity, but seeks to provide an indication of the likely position of the development within current market expectations.

The outcomes of the consultation exercise suggest the required charges are within the market range for quality industrial facilities in each of the locations under consideration.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Stakeholders suggested there is very limited supply, in particular of larger sites, and that tenants are likely to be willing to pay a premium to access high quality lots.

The analysis found the development would be feasible at several potential locations, and there is strong demand for high quality industrial land throughout the Central Queensland region. These findings are supported by the limited availability and high prices paid for sought after locations when they do become available. However, demand and willingness to pay declines rapidly for sub-prime sites where space may be cramped, lots are smaller than would be preferred, or where there are potential conflicts of use issues.

Location Analysis

Five potential locations were considered for the logistics hub: Parkhurst and Gracemere (on the outskirts of Rockhampton), Emerald, Gladstone (outside the GSDA1) and Gladstone (within the GSDA). With the possible exception of Parkhurst and the GSDA, Gracemere, Emerald and Gladstone each has the potential to accommodate a viable logistics hub. The location decision is likely to be determined by the value an organisation places on the location benefits of Gladstone (e.g., deep water access, existing related businesses) and Emerald (e.g., proximity to mine sites and existing mining services sector), and whether this is sufficient to offset the lower land and labour costs associated with the Gracemere site.

Gladstone's location adjacent to one of Queensland's major deep water port facilities would offer the opportunity to run loads from ship to destination without the need to add an additional handling point. This would reduce costs between the point of loading and the point of delivery. However, as well as having relatively high land costs and limited availability, a Gladstone location would also incur significant additional labour costs, assuming appropriate labour resources could be found. It is unlikely the value derived from a Gladstone location would offset the higher establishment and operating costs. While Emerald is at the heart of the Bowen Basin it is unlikely to be a viable location for non-resource based logistics businesses. It also has higher land and labour costs than alternative locations.

The Gracemere site at Rockhampton West was identified as the preferred location. It offers the opportunity to meet immediate demand from the mining services sector and the longer term aim of creating a viable intermodal facility. Gracemere is the preferred location given its relatively low land costs, potential for direct rail line access, greater availability of labour at a lower cost, and its location at the point at which larger vehicles are permitted from the west.

It is recommended CQILH Incorporated:

Move to a full feasibility stage including a detailed assessment of the feasibility of the

logistics hub at the Gracemere industrial land development to the west of Rockhampton;

Initiate a market sounding campaign to gather expressions of interest in the site as a

means of communicating to the business community that the development is progressing, and as a sign to the development community that demand is strong and the development is feasible; and

Continue to engage with rail infrastructure providers to signal the commitment to the

incorporation of road: rail interchange handling capacity at the site over the medium term.

1 Gladstone State Development Area.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Table of Contents

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

1. Introduction and Background

Background

Central Queensland is experiencing a period of ongoing economic and population growth closely linked to its abundant natural resources. The transport industry has a critical role in enabling ongoing development and the potential opportunity to establish an intermodal logistics hub in Central Queensland has been discussed for several years.

Central Queensland's location relative to three major natural resource areas, the well established agricultural sector and ability to service the north, south and west of Queensland suggest such a development might provide a viable opportunity. However, the initial capital investment required is significant.

Need for the Study

It is envisioned an intermodal hub would provide a critical piece of regional transport infrastructure, increase efficiency in the sector and help ensure the regional economy is not constrained by high costs. However, the development will only proceed where there is sufficient demand to make the facility commercially viable. AECgroup was engaged to undertake a pre-feasibility analysis of the opportunity. The assessment has been conducted in two parts:

Baseline Analysis (Chapter 2-6): summarises the regional demographic and

economic profile, planning context, case studies of similar facilities and potential demand. The analysis concludes by identifying the features of a viable facility; and

Pre-Feasibility Assessment (Chapter 7-9): sets out a pre-feasibility assessment

for a potential facility.

Approach Used

The baseline analysis (chapters 2-6), uses the following structure:

Central Queensland Catchment Profile: provides an overview of the demographic

and economic profile of the catchment, focussing on implications for the transport sector;

Strategic Freight Planning Context: identifies the key planning strategies

influencing the freight transport sector in Central Queensland;

Current Freight Task: describes the freight task in the region and the contributions

of rail, road and sea freight;

Opportunity for an Intermodal Facility: describes of trends in intermodal facilities

and an assessment of demand for a Central Queensland Intermodal facility; and

Demand for a Logistics Hub: assesses the features which could be included in a

viable road based logistics hub.

The pre-feasibility assessment (Chapters 7-9), uses the following structure:

Facility Description and Demand Assessment: describes the facility and

discusses the key drivers of demand for each component;

Pre-Feasibility Assessment: assesses the anticipated costs of establishing the

required facility and the likelihood these could be borne by the market;

Location Analysis: identifies a set of critical location criteria and assesses potential

locations to identify which best meets the needs of the facility; and

The report concludes with findings and recommendations (Chapter 10) from parts A &

B.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

2. Catchment Profile

Key Findings and Implications:

In 2011, the estimated resident population of the Fitzroy SD was 228,382 and this is

anticipated to increase to 343,669 by 2031, an increase of 115,287.

Population growth has historically been lower than the Queensland average, however

future growth, between 2011 and 2031, is projected to be higher than Queensland's, with an average annual growth rate of 2.1% within the Fitzroy SD compared to 1.8% for Queensland.

Gladstone Regional Council (2.9%) and Central Highland Regional Council (2.4%) are

projected to record the highest population growth rates within the Fitzroy Statistical Division (SD) between 2011 to 2031.

‘Technicians and trade workers' was the largest occupational group within the Fitzroy

Three of the five LGA's (Local Government Areas) in the catchment (Banana, Central

Highlands and Gladstone) recorded average annual incomes greater than $50,000 per year.

By 2031, the Fitzroy SD will need to almost double its number of dwellings, requiring

an additional 1,700 to 2,700 dwellings a year.

The Gross Regional Product of the Fitzroy SD is $17.1 billion, contributing

approximately 6.4% of Queensland's Gross State Product.

Mining is the largest industry within the Fitzroy SD, contributing 28.7% of Gross

Value Add2, with the contribution being as high as 60.1% and 70.0% in the Banana and Central Highland Regional Council areas.

It is anticipated the ongoing expansion and operation of the resources sector will

continue to act as the key driver of economic activity in the Central Queensland region including direct mining activity as well as the associated service industries.

The Fitzroy SD has a labour force of approximately 121,000 people, with an

unemployment rate of 5.5%.

Catchment Definition

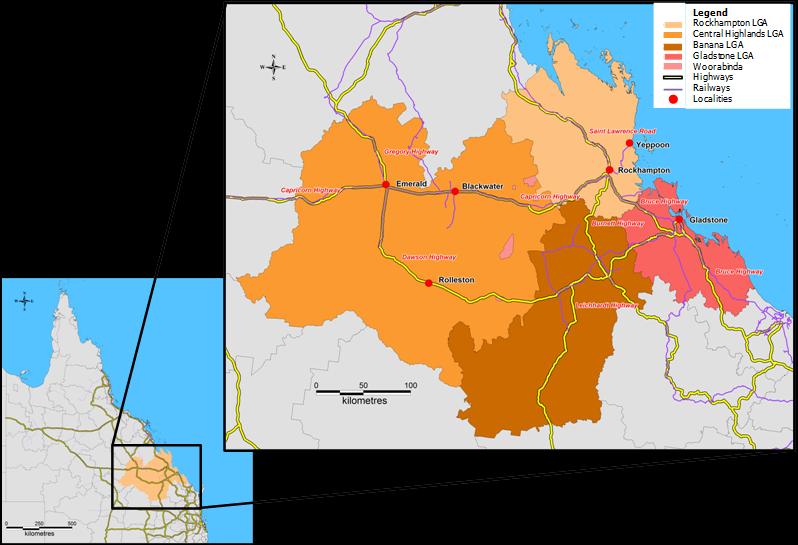

The following table and map introduce the local government areas (LGA's) that make up the catchment for the economic and demographic profiles - the Fitzroy Statistical Division (SD).

Table 2.1. Local Government Areas in Fitzroy SD

Local Government Area

Estimated Residential

Population (2010)

(square kilometres)

Central Highlands LGA

Fitzroy SD

Source: ABS (2011a)

2 Gross Value Add is the total value generated by the industries within the economy, excluding

ownership of dwellings

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 2.1. Local Government Areas in Fitzroy SD

Source: AECgroup

Demographic Profile

Population Growth

The following figure and table summarise the historic and projected population estimates for the LGA's within the Fitzroy SD.

Figure 2.2. Fitzroy SD Population Projections

Central Highlands

Source: ABS (2011a), Queensland Treasury (2011), DIP (2008).

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Between 2011 and 2031, Gladstone LGA is projected to experience the largest growth in population with an average annual population growth of 2.9%, followed by Central Highlands LGA with 2.4% average annual population growth. These high projected population growth rates are considered to be largely due to the sustained high level of investment in manufacturing (Gladstone) and mining (Central Highlands).

The Rockhampton LGA's population is projected to increase by more than 50,000 between 2011 and 2031 and to remain the LGA with the highest population within the Fitzroy SD, containing approximately half of the region's population.

Table 2.2. LGA Population Growth 2006-2031

LGA

Population

Banana

Central Highlands

5 Year Average Annual Population Growth Rate

Banana

Central Highlands

Source: ABS (2011a), Queensland Treasury (2011), DIP (2008).

Employment by Occupation

In 2006, the Fitzroy SD contained a high proportion of technicians and trade workers compared to other occupations. The large number of technicians and trade workers, as well as the large proportion of labourers and machinery operators and drivers is consistent with regions containing heavy industries such as mining and manufacturing.

The large number of managers within the Fitzroy SD is indicative of the continued importance of the region's large agricultural base and the number of agricultural/farm owners. In contrast, the Fitzroy SD contains a relatively small number of community and personal service workers and sales workers.

Table 2.3. Employment by Occupation, Place of Work, Fitzroy SD

Occupation

Employees % Employed

Technicians and trades workers

Community and personal service workers

Clerical and administrative workers

Machinery operators and drivers

Source: ABS (2007b)

Average Incomes

In 2010-11, within the Fitzroy SD, the Central Highlands LGA recorded the highest average yearly income ($64,291), thought to be driven by the higher incomes within the resources sector. This was followed by the Gladstone LGA ($57,654) and the Banana LGA ($56,231).

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 2.3. LGA Estimated Average Yearly Income, 2010-11

Central Highlands

Source: ABS (2011b), ABS (2011c)

Dwelling Projections

It has been estimated that by 2031 the Fitzroy SD will require approximately 60,000 new dwellings to accommodate future population growth. This required increase in new residential dwellings indicates the potential for future construction activity within the region over the next 20 years. On this basis, the Fitzroy SD will require an additional 1,700 to 2,700 dwellings per year between 2011 and 2031 to meet projected demand.

Figure 2.4 Dwelling Projections, Fitzroy SD (2006 to 2031)

Fitzroy Statistical Division

Source: AECgroup

Economic Profile

Population

The Fitzroy SD had a population of 206,204 people in 2006, which had increased to 223,516 by 2010. Between 2006 and 2010, the population of the Fitzroy SD grew at a slightly lower rate than the Queensland average, however, the Fitzroy SD is projected to

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

grow at a faster rate than the state average up until the year 2031, adding approximately 115,000 people to the region's population.

Table 2.4. Historic Catchment Population and Projected Growth

Region

Historic Population

Population Projections

Average Annual Growth

2031 2006-11 2011-16 2016-31

Queensland 4,090,908 4,513,850 5,105,892 5,602,920 6,609,730

Source: ABS (2011a), Queensland Treasury (2011), DIP (2008).

The Fitzroy SD has seen steady population growth of approximately 2.0% per year over the past four years, with the annual growth rate reaching as high as 2.4% in 2009. In 2010, there was a reduction in the population growth rate to 1.3%, however the rate is projected to return to approximately 2.4% over the next several years before gradually falling to 2.0% from 2016 to 2031.

Figure 2.5. Forecast Population Growth, Fitzroy SD

Fitzroy SD Population

Fitzroy SD Populatin Growth Rate

QLD Population Growth Rate

Source: ABS (2011a), Queensland Treasury (2011), DIP (2008).

Gross Regional Product

The Fitzroy SD is estimated to have generated a gross regional product (GRP) of $17.1 billion in 2010-11, equating to approximately 6.4% of the Queensland's gross state product (GSP). The Fitzroy SD's GRP is estimated to have grown by 8.8% per annum between 2006-07 and 2010-11, well above the Queensland economy's growth rate of 5.7% per annum in the same period.

Table 2.5. Gross State/ Regional Product

Region

GRP/ GSP ($M)

Fitzroy SD (GRP)

Queensland (GSP)

Source: AECgroup.

The following table summarises the contribution of each industry sector to the total industry value add3 in the Fitzroy SD and Queensland during 2010-11. Mining makes the largest contribution to the SD's economy, accounting for almost a third of total industry

3 Industry Value Add is the total value of outputs produced by each industry contributing to the

Gross Regional Product for a region.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

value added activity, 2.97 times higher than the contribution of the industry to the total Queensland economy. Similarly, manufacturing makes up just under 13.7% of the SD's economy, 1.76 times larger than the contribution of the industry to the Queensland total.

Information, media and telecommunication and arts and recreation services are the two smallest industries in the Fitzroy SD, accounting for 0.5% and 0.1% of the SD's economy respectively. The industries make 0.27 and 0.18 times the contribution to the Fitzroy SD's economy than they make to the Queensland economy.

Table 2.6. Industry Contributions to Total Gross Value Add in the Study Area and

Queensland, 2009-10

Industry

Fitzroy SD

Queensland

Location

Quotient (a)

Agriculture, forestry and fishing

Electricity, gas, water and waste services

Accommodation and food services

Transport, postal and warehousing

Information media and telecommunications

Financial and insurance services

Rental, hiring and real estate services

Professional, scientific and technical services

Administrative and support services

Public administration and safety

Education and training

Health care and social assistance

Arts and recreation services

Ownership of dwel ings

Total Industry Value Add

$248,936

Taxes less Subsidies

Gross Regional Product

$266,736

Note: (a) Location Quotient represents each industry's percent contribution to total Study Area GVA divided by the industry's contribution to Queensland GVA and represents the relative strength of each industry compared to Queensland as a benchmark. A

location quotient of between 0 and 1 indicates an industry represents a lower proportion of the overal Study Area economy compared to Queensland. The closer the location quotient is to 0, the smal er the industry's contribution comparative to the

Queensland benchmark. Conversely, a location quotient above 1 indicates an industry represents a higher proportion of the Study

Area economy compared to Queensland. Source: AECgroup.

The following table breaks down the industry contribution to GRP within each LGA in Fitzroy SD.

Table 2.7. Industry Contributions to Total Gross Value Add, 2010-11

Industry

Agriculture, forestry and fishing

Electricity, gas, water and waste services

Accommodation and food services

Transport, postal and warehousing

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Industry

Information media and telecommunications

Financial and insurance services

Rental, hiring and real estate services

Professional, scientific and technical services

Administrative and support services

Public administration and safety

Education and training

Health care and social assistance

Arts and recreation services

Ownership of dwel ings

Total Industry Value Add

Taxes less Subsidies

Gross Regional Product ($m)

Notes: RRC Rockhampton LGA, GRC Gladstone LGA, CHRC - Central Highlands LGA, BRC - Banana LGA, WRC - Woorabinda LGA

Source: AECgroup.

The transport, postal and warehousing sector accounts for 8.6% and 10.7% of the Rockhampton and Gladstone economies respectively, much higher than the 2.9% to 2.1% in the remaining LGA's. Rockhampton has the most diverse economy, with the manufacturing and health care and social assistance industries being the largest contributors to the LGA's economy, despite each only contributing 10.1%. The Central Highlands and Banana LGAs are both heavily reliant on the mining industry, which accounts for 70.0% and 60.1% of their local economies respectively. Manufacturing (37.7%) is by far the biggest contributor to the Gladstone LGA's economy.

GRP Growth Drivers

Future GRP is likely to be influenced by several macro-economic factors and is difficult to forecast with accuracy given the high degree of uncertainty in particular over the long-term. However, the available data strongly supports the expectation of high levels of continued growth in the resources and related sectors in the Central Queensland economy.

2.3.3.1 Mining Production

Coal production within Central Queensland area is expected to grow significantly over the short to medium term. Forecasts show that by 2030 the Queensland production of coal is expected to peak at approximately 340 million tonnes annually, equating to production increasing by approximately 5.5% per annum (Department of Infrastructure and Planning, 2010). Given the location of the Fitzroy SD and its positioning relative to the Surat, Bowen and Galilee Basins, much of this future expansion is anticipated to occur within or close to the Fitzroy SD, subsequently resulting in direct and indirect increases in GRP.

2.3.3.2 Agricultural Production

Grain production within Central Queensland is forecast to remain relatively stable over the coming years, in line with the ABARES (2011) estimates for Australia. The main factor for grain production which will affect the Fitzroy SD's GRP will come as a result of changes in the price for grain. Increased demand from developing countries, driven primarily from East Asia as well as North Africa and the Middle East for wheat and sorghum has resulted in the world price increasing in the short term, however decreasing in the mid to long term as world supply begins to increase. These factors will result in the nominal value of grain produced to increase within the Fitzroy SD, however the output is forecasted to remain relatively steady in the short to medium term.

The production of livestock, specifically relating to cattle within the Fitzroy SD is forecast to increase from restocking as a result of the increased availability of feed caused by the recent above average rainfall within Central Queensland.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Labour Market Characteristics

2.3.4.1 Labour Force and Employment

The Fitzroy SD's unemployment rate was 5.7% in the June quarter 2011, approximately 2.0 percentage points higher than the corresponding quarter in 2007.

Table 2.8. Labour Market Characteristics, June Quarter 2007 to June Quarter 2011

Region

Unemployed Labour Force Unemployment Rate

Fitzroy SD

June 2007

Average Annual % Growth 06-10

Queensland

June 2007

Average Annual % Growth 06-10

Source: DEEWR (2011).

The following figure shows the Fitzroy SD's labour force has increased significantly over the past five years, with over 10,000 people being added over this period. The last three quarters have seen growth of 5.5% or approximately 6,300 people.

The SD's unemployment rate has steadily risen over the past few years from a low of 3.3% in the September 2007 quarter. Unemployment has fluctuated between 5% and 6% since the March 2009 quarter, reaching a high of 5.9% in the December 2009 quarter.

Figure 2.6. Labour Force and Unemployment Rate, Fitzroy SD

Fitzroy SD Labour Force

Fitzroy SD Unemployment Rate

QLD Unemployment Rate

Source: DEEWR (2011).

The following figure shows the unemployment rates over the past five years of the individual LGAs that make up the Fitzroy SD. The Rockhampton LGA had the highest unemployment rate of the LGAs with unemployment fluctuating between 6.5% and 7.0% over the past two years. The Banana LGA has the lowest unemployment rate in the region, with unemployment being recorded at 3.2% in the June 2011 quarter. The LGA's unemployment rates all follow a similar pattern, recording lows towards the end of 2007 before steadily rising until the December 2009 quarter.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 2.7. Figure 2.6 Unemployment Rates, Fitzroy SD

Central Highlands + Woorabinda

Source: DEEWR (2011).

Employment by Industry

The three largest industries by employment in the Fitzroy SD are ‘retail trade', ‘manufacturing' and ‘health care and social assistance', which is similar to the State wide average. However, relative to the Queensland average the Fitzroy SD has particularly large ‘mining' (location quotient of 4.23), ‘electricity, gas, water and waste services' (location quotient of 2.32) and ‘agriculture, forestry and fishing' (location quotient of 1.55) industries. The smallest industry in the catchment relative to state wide average is the ‘arts and recreation services', which recorded a location quotient of 0.45.

Table 2.9. Employment by Industry, Place of Work, Fitzroy SD (2006)

Employment by Industry

Fitzroy SD

Queensland Location Quotient

Agriculture, forestry and fishing

Electricity, gas, water and waste services

Accommodation and food services

Transport, postal and warehousing

Information media and telecommunications

Financial and insurance services

Rental, hiring and real estate services

Professional, scientific and technical services

Administrative and support services

Public administration and safety

Education and training

Health care and social assistance

Arts and recreation services

1,737,619

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Note: (a) The Location Quotient represents each industry's percent contribution to total employment in the Study Area divided by

the industry's contribution to Queensland's total employment and represents the relative proportional size of workforce for each industry compared to Queensland as a benchmark.

Source: ABS (2007a), AECgroup

The following figure shows the breakdown of the ten largest industries in the catchment area by employment. Approximately half of the catchment area's labour force is employed in the five largest industries.

Figure 2.8. Industry of Employment, Place of Work, (2006)

Health care and social assistance

Education and training

Accommodation and food services

Transport, postal and warehousing

Public administration and safety

Agriculture, forestry and fishing

Source: ABS (2007a)

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

3. Strategic Freight Planning Context

Key Findings and Implications:

There is increasing recognition of the need for an integrated freight network

throughout Queensland, and Australia, in order to:

Avoid duplication of key infrastructure;

Identify infrastructure gaps; and

Increase productivity.

Transport infrastructure has a key role in regional development activity.

Forward thinking provision of land for industrial growth and freight corridors is

Partnerships between all levels of government and industry are required to achieve

optimal outcomes.

Consideration of environmental factors (including sustainability, greenhouse gas

emissions and air quality) is increasing and is likely to continue to do so.

The following sections summarise the implications of a series of key documents including:

Queensland Regionalisation Strategy;

Integrated Freight Strategy for Queensland;

Brisbane–Cairns Corridor Strategy;

National Land Freight Strategy Discussion Paper;

Queensland Infrastructure Plan;

Bruce Highway Upgrade Strategy;

Transport Coordination Plan for Queensland; and

Queensland Coal Transport – Coal Infrastructure in Queensland.

Summaries of the documents reviewed are provided in Appendix A.

Queensland Growth

Queensland has one of the fastest growing economies in Australia, unpinned by growth in the mining and energy sectors. Workers are moving into the State from interstate and overseas to take up jobs. Population growth is strong and expected to continue, with an additional 2.5 million people forecast to live in Queensland by 2031 (DLGP, 2011c).

A major challenge for the Queensland Government is to actively manage the impacts of this growth. By investing in infrastructure and services to support growth in regional areas, people will be encouraged to settle outside of South East Queensland. Attracting workers to regional Queensland, where and when they are needed, is an essential part of the Government's population growth strategy.

Primary industries are economically important in Central Queensland. Grazing is a major industry with Rockhampton promoting itself as Australia's beef capital. Currently, the mining and energy industries are strong drivers of population growth and investment. The region is rich in high quality coking coal, much of which is exported through the Port of Gladstone. Central Queensland also produces a significant amount of the state's electricity from the Stanwell, Gladstone and Callide power stations (DEEDI, 2011). The infrastructure requirements to meet the growing needs of the region are substantial. Significant public and private sector investment is already occurring in the region (e.g. Port of Gladstone expansions). There is increasing pressure on transport infrastructure, community resources and utilities to meet industry demands.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Impacts of Infrastructure Investment on Productivity

The total value of known investment projects in Queensland, either committed or under construction, surpassed $78 billion in the March quarter 2011, the highest on record (DLGP, 2011b). Infrastructure investment drives productivity and competitiveness by reducing the costs of doing business, and finding new ways of producing and delivering goods and services. It is estimated that each dollar of infrastructure investment boosts economic activity by between $1.00 and $1.60. The International Monetary Fund estimates gross domestic product (GDP) multipliers from infrastructure investments can be as high as 1.8 (DPLG, 2011b).

Productivity and competitiveness are inhibited by constraints to freight (Infrastructure Australia, 2011). This was highlighted by the 2011 floods and cyclones, which affected numerous rail and road freight routes throughout Queensland. ABARES (2011) estimates that Queensland's coal exports between December 2010 and March 2011 reduced export earnings by around $2.0–2.5 billion.

Australia's total freight task will double between 2006-2020 and triple by 2050 (Mirvac, n.d.). Transport networks must be efficient – every 1.0% increase in productivity to the freight transport network saves the economy $1.5 billion (Mirvac, n.d.). In Queensland, the challenge lies in accommodating this rapid growth in freight when exposure to ageing, inadequate infrastructure including sections of the Bruce Highway and the North Coast Railway are high.

Impacts on Central Queensland

Freight management trends are towards higher efficiency freight solutions focused on faster freight carriage and transfer, low inventory levels, automated warehousing and integrated logistics systems (Mirvac, n.d.). The Queensland and Australian governments recognise the importance forward planning and integrated transport strategies (DLGP 2011b, DLGP 2011c, DOTARS 2007, Infrastructure Australia 2011, TMR 2008, TMR 2010). In Central Queensland, direct air and freight routes make Rockhampton the key logistics and freight hub connecting the Capricorn and Bruce highways. Proximity to the Bowen Basin makes Rockhampton a key service and logistics hub for the coal industry, providing road, rail and air services.

The Rockhampton Regional Council (2010) outlines strategic economic, environmental and social goals for the region. This includes making Rockhampton a prosperous and self sustaining region through:

Effective infrastructure management that delivers ongoing growth; and

Regional development that occurs as a result of increased investment and the

attraction of new, diverse industries.

These goals align to Queensland Infrastructure Plan (QIP) (DLGP 2011b) which include:

Upgrades to the Dawson, Leichhardt, Bruce, Capricorn and Landsborough highways.

A planning project will be finalised in 2011–12 to investigate options to improve the flood immunity of the Bruce Highway between the intersection with the Burnett Highway and Rockhampton;

Improving heavy vehicle access in Rockhampton to the Bruce Highway, facilitate the

Surat Basin Rail project, improve freight access to the Gracemere Stanwell Industrial Corridor, improve freight movement efficiency to and from the Surat Basin, respond to resource growth in the Galilee Basin, support economic and urban growth in key regional centres, and facilitate and manage freight between the Port of Gladstone and industrial precincts; and

Developing and improving access to the Stanwell Gracemere Industrial Corridor.

Enabling industrial development at this location will require significant investment in transport.

Transport Externalities

All modes of transport impose external costs on the community and the transport network. Transport externalities are generally:

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Environmental (e.g., GHG emissions, air quality issues); or

Social: (e.g., congestion, wear and tear on roads, noise, accidents).

External costs are significantly lower for rail transport compared to road. In planning future infrastructure, the impact of these costs on modal choice and route are likely to be the source of significant future debate (TMR, 2009).

Transport produced 14.8% Australia's GHG emissions in 2009 and is one of the fastest growing sources. Between 1990 and 2009, transport emissions grew by 34.6%. While most emissions are associated with personal travel, those from freight are increasing at a higher rate (DCCEE, 2011).

Climate change policy suggests that freight should increasingly shift from road to rail where possible. Rail requires one third of the amount of fuel and produces less than one third of the emissions compared to road transport. One freight train between Melbourne and Sydney replaces 150 semi-trailers, saves 45,000 litres of fuel, and 130 tonnes of GHG emissions (OEH, 2011).

Australia's overarching climate change policy is the Carbon Price Mechanism (CPM). The CPM will place an impost on every tonne of GHG emissions produced by large emitters from 1 July 2012. For the first three years, the carbon price will be fixed. It will then transfer to an emissions trading scheme (ETS) on 1 July 2015 (Australian Government, 2011).

Transport fuels used in domestic aviation, domestic shipping, rail, off-road transport and non-transport use of fuels are covered under the scheme. Transport fuels used by for on-road transport by vehicles are excluded. The government is proposing to include heavy vehicles in the scheme from 1 July 2014, however, this has not been agreed to by all members of the Multi-Party Climate Change Committee. The impact of a carbon price on the freight industry remains unknown.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

4. Central Queensland Freight Task

Key Findings and Implications:

There has been a very large increase in the total freight task across all modes of

transport and in particular road and rail.

Not all commodities can be carried efficiently by all transport modes.

Intermodal logistics facilities are characterised by the need for large, continuous,

throughput volumes.

Inland ports have been successfully established in several countries and these are

reliant upon high quality road and rail connections to major port facilities and close proximity to large markets.

In Australia, major intermodal facilities tend to be located at the major port facilities

although smaller road and rail facilities are beginning to emerge associated with the development of large industrial areas which provide a ready source of freight flows in to and out of the facility.

Intermodal facilities can act as a keystone for other transport and industrial

Several intermodal facilities have reached feasibility planning stages but have not yet

proceeded to implementation.

Australian Freight Task

Prior to the 1960s, rail was the predominant form of land-based freight transport in Australia. Through improving infrastructure and capabilities of road transport since this time, road freight transport has grown significantly, although rail still remains a significant form of freight transportation. In 2007, total Australian freight levels reached 521 billion tonne kilometres, of which 40.0% was transported by rail. These levels had doubled over the previous 20 years, averaging 3.5% growth annually (BITRE, 2009). Between 2005 and 2030, both rail and road freight is expected to double again, at an average growth of 3.0% annually (BITRE, 2009). The growth in rail freight is largely based on the minerals and resources boom increasing demand for bulk haulage, whilst road freight growth is largely underpinned by manufactured goods.

Figure 4.1. Long Term Australian Freight Trends

Source: Department of Infrastructure and Transport (2009)

Rail freight largely comprises of bulk freight, defined as large quantities of homogenous goods. These goods are usually characterized by being a high quantity, low value

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

product. Rail accounted for 48% and shipping 36% of the bulk freight services in 2006-2007, with major cost benefits in rail transport over road transport in coal and iron ore (BITRE, 2009). During this period, the rail task totaled 102 billion tonne kilometers, of which 67.6 billion tonne kilometers was bulk freight, and 34.4 billion was intermodal freight (BITRE, 2008). This increased significantly in the 2007-08 period, with total task at 197.6 billion tonne kilometers, of which 171.7 billion was bulk freight and 25.9 billion was intermodal freight (BITRE, 2010).

In some bulk products, such as grains, sands and uranium, road and rail can both compete and cooperate in freight transport. Whilst rail freight is a cost effective option when the required infrastructure is in place, where it is not, road transport can effectively compete with rail, and act as a link between the rail infrastructure and the departure point of the good.

Significant economies of scale are also present for rail in terms of cost related to volume and distance travelled. This gives the rail freight mode a significant advantage over the road freight mode over longer distances, as road transport costs per distance are largely fixed. This is compounded by the rising oil prices driving cost per distance up for road transport at a higher rate than rail freight costs (BITRE, 2009). This gives a significant advantage to rail freight transport in the future given that oil price trends continue to rise. Rail is however hindered by the inability to service freight to locations beyond the infrastructure in place.

The Central Queensland Blackwater Coal System is the largest system operated by QR National and carries the second highest tonnages on the network. The System services the Bowen Basin linking mines to the export terminals at the Port of Gladstone. The Blackwater System also services domestic users including Stanwell and Gladstone Power Station, Cement Australia and the Comalco Refinery. The Port of Gladstone has stockpiling facilities which provide some supply flexibility. The System is a mix of electrified and non-electrified track including single and duplicated sections. At the Port of Gladstone QR National has a dangerous cargo spur line and direct access to the port and its container facility.

In 2010-11, a year in which production was significantly reduced due to flooding, the Blackwater System still hauled a total of 45.8 million tonnes of coal, having previously moved in excess of 50 million tonnes in previous years. A range of macro-economic factors, coupled with planned infrastructure investments, indicate the volume of coal moved will continue to increase over the medium to long-term and that track capacity will be the limiting factor rather than demand.

Other Freight

The North Coast Line system is the principal freight and passenger line within the Queensland Rail network, running the length of Coastal Queensland between Brisbane in the south and Cairns in the north, a distance of 1,680 km. The system caters for all traffic tasks including containerised freight services, high speed tilt trains, commuter services, heavy haul single commodity trains of sugar, grain or minerals and cattle trains. Freight services are operated by QR National and Pacific National. The North Coast Line system carries in excess of 11.0 million tonnes of various products annually (QR National, 2012).

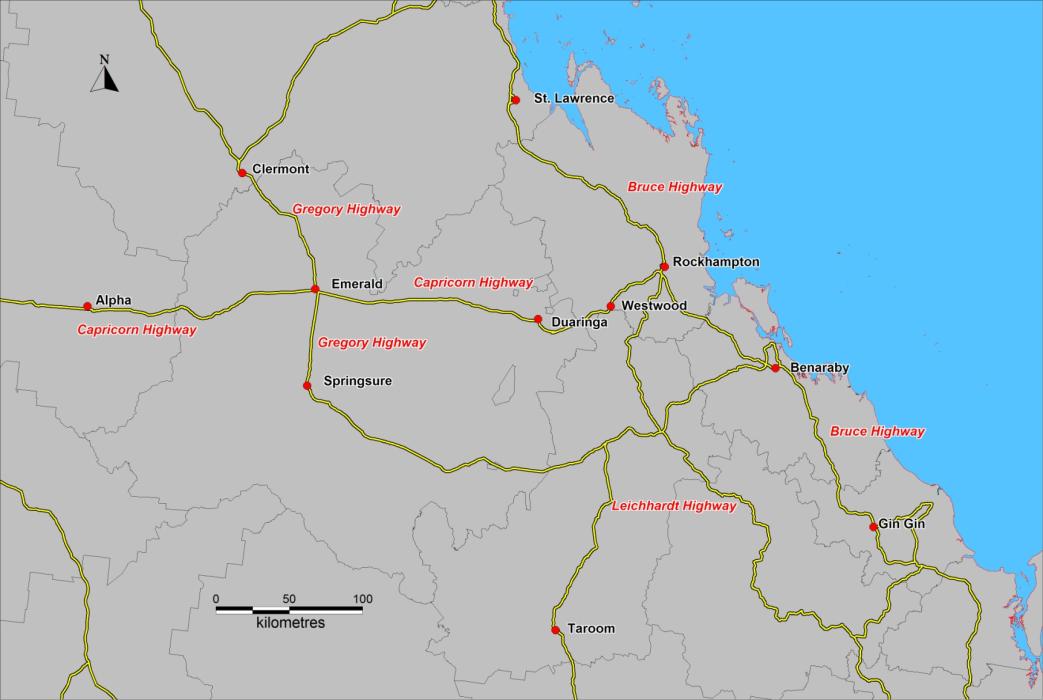

Traffic Counts

The Department of Transport and Main Roads collect traffic data for principle routes around Queensland and have provided data for selected routes in Central Queensland which are highlighted in the following figure.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 4.2. Central Queensland Traffic Count Routes

Source: TMR (2011)

The average daily traffic flow of heavy vehicles along the Bruce Highway between Gin Gin and Rockhampton was between 600 and 1,100 heavy vehicles per day, depending on the section of highway. The heavy vehicle numbers along the Bruce Highway peak entering Rockhampton and north of Gladstone, with over 1,000 vehicles per day travelling along this route. In contrast, vehicle numbers along the Bruce Highway drop to their lowest levels along the Bruce highway to the south of Gladstone. This indicates that a large proportion of regional freight flows between Gladstone and Rockhampton.

The average annual number of heavy vehicles what travel between Rockhampton and St. Lawrence average between 400 and 800 vehicles, depending on the segment of road. The number of heavy vehicles travelling along this route gradually decreases from a maximum of 770 just north of Rockhampton to 423 at the Rockhampton-Mackay Shire Boundaries.

West from Rockhampton, along the Capricorn Highway, total heavy vehicle numbers between Rockhampton and Alpha are constant along the majority of the highway, with decreases in traffic volumes offering at major intersections. Between Rockhampton and Duaringa, the average annual daily number of heavy vehicles is approximately 350. This number decreases after Duaringa, where vehicles turn off the Capricorn Highway onto the Fitzroy Development Road, accounting for approximately 100 heavy vehicles. The number of heavy vehicles remaining on the Capricorn Highway does not significantly change until the road reaches Emerald, where the Capricorn Highway intersects with the Gregory Highway, which accounts for another large decrease in heavy vehicles travelling along the Capricorn Highway. After this point, the number of heavy vehicles slowly decreases until Alpha.

Heavy vehicles along the Gregory Highway, between Springsure in the south and Clermont in the north, were highest around Emerald, with total annual average vehicles amounting to 237 heavy vehicles to the north of Emerald. In contrast, Springsure recorded 10 heavy vehicles per day. This indicates that the vehicles which travel along the Gregory Highway between Springsure and Clermont originating from either the Capricorn Highway or to the north of Clermont.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 4.3 Central Queensland Total Average Daily Traffic Counts

Highway Route

Midpoint

Distance

Vehicle Counts

Bruce Highway

(Gin Gin to Rockhampton)

(Rockhampton to St. Lawrence)

Capricorn Highway (Rockhampton to Alpha)

Leichhardt Highway

(Westwood to Taroom)

(Springsure to Clermont)

Tonnage

Bruce Highway

(Gin Gin to Rockhampton)

(Rockhampton to St. Lawrence) Capricorn Highway (Rockhampton to Alpha)

Leichhardt Highway

(Westwood to Taroom)

Gregory Highway (Springsure to Clermont)

Source: Queensland Government Department of Transport and Main Roads (2010) Traffic Analysis and Reporting System, AADT Segment Reports, Traffic Year 2010, Queensland Government, Brisbane

Port Volumes

Much of the freight moving around the Central Queensland region is heading for or coming from the Port of Gladstone, and to a lesser extent Port Alma. The following sections summarise the type and volume of freight imports and experts at each facility between 2007 and 2011.

Port of Gladstone

The following figure shows the tonnage of exported goods from the Port of Gladstone. The port is predominantly used for exports, with approximately 80% of the tonnage traffic consisting of exports.

Figure 4.4. Export Tonnage – Port of Gladstone

Aluminium Products

Source: Port of Gladstone

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Coal accounts for the majority of exports, contributing to an average of 56 million tonnes (over 85% of total) of exports annually. Coal exports between 2008 and 2010 showed consistent growth (5.21%, 3.29%, and 6.37% respectively), with 2011 showing a decline as a result of the January floods and associated production delays.

Aluminium and alumina are the second largest exports, averaging four million tonnes annually. Cement products and other exports make up less than five percent of the total exports with tonnage of under two million annually most years over the five year period.

The following figure summarises the import tonnage into the Port of Gladstone. As reflected in exports, 2011 shows a significant reduction in total imports following the January floods.

Figure 4.5. Import Tonnage – Port of Gladstone

Petroleum/LPG Products

Source: Port of Gladstone

Bauxite is the largest import into the port, with an average of 12.3 million tons imported annually. This represents 79% of total import tonnage, with petroleum and LPG products, caustic soda, and other products making up the remaining 21% of imports.

Before 2010, bauxite imports were increasing at an average of 2.51%, after which bauxite imports declined in 2010 (3.25%) and 2011 (27.89%). Caustic soda, and Petroleum and LPG product imports are the second and third largest imports to the port averaging 1.46 million tons (9.39%) and 1.23 million tons (7.93%) respectively over the five year period. Caustic soda imports grew by approximately 5% between 2007 and 2011, with petroleum and LPG imports over the five years showing an average growth rate of 4.43%. Both caustic soda, and petroleum and LPG product imports continued to grow in the 2011 by 4.79% and 9.34% in contrast to the contraction of bauxite imports in the same year.

Port Alma

Port Alma shipping traffic is largely dominated by ammonium nitrate movements in and out of the port. The following figure demonstrates that over a 5 year period between 2007 and 2011, bulk-bagged ammonium nitrate accounted for 76.22% of export traffic in the port, with an average of 102,083 tons per year.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 4.6. Export Tonnage – Port Alma

B'Bulk Bag - Ammonium Nitrate

Source: Port of Gladstone

Over the 5 year period there was an average export growth rate of 2.72% in ammonium nitrate, with the peak traffic by tonnage in 2009 at 113,671 tons. The only other export of significance in the port is tallow, of which the average tonnage per year was 28,055, and a growth rate of 1.06% over the five year period.

Imports into Port Alma also largely consist of ammonium nitrate shipping, with a recent increase in petroleum and bio fuels imports in the last three years.

Figure 4.7. Import Tonnage – Port Alma

B'Bulk Bag - Ammonium Nitrate

Petroleum / Bio Fuels

Source: Port of Gladstone

Ammonium nitrate imports over the five years averaged at 72,545 tonnes annually, at a growth rate of 25.2%. This growth was characterised by a large growth of 102.6% between 2007 and 2008 and a contraction in import tonnage of 24.80% between 2010 and 2011. The import of petroleum and bio fuels into the port from 2009-2011 grew rapidly, at an average rate of 94.5% over the three years to reach 75,777 tonnes per year. The other significant feature of imports over the 5 year period was the increase in other shipping imports in 2011, largely due to salt imports of 67,936 tons during the year.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

There are already significant freight movements in the region and these are forecast to continue to increase. Freight is transported by road, rail, and sea as well as a small volume by air. The choice of mode is determined by the characteristics of the commodity to be transported including its size, uniformity, value as well as its destination. It is important to recognise that not every commodity is suitable for transport by every available mode.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

5. Opportunity for an Intermodal Facility

Key Findings and Implications:

There are existing facilities with intermodal capability in the Central Queensland

region which appear to operate on a financially viable basis.

These facilities have significant site constraints and conflict of use issues but both

sites also have major sunk costs.

Much of the current and forecast increase in freight in the region is not suitable for

intermodal transport.

There are a series of currently unknown factors that may improve the feasibility of an

intermodal facility over the medium to long-term.

Unless the existing operators were compensated for their sunk investments, the

intermodal component of the facility is not considered viable and should not be considered further in the pre-feasibility study.

The remainder of the study should focus upon a road based logistics precinct.

Trends in Intermodal Transport

Current National Issues

In the past, infrastructure planning has often paid insufficient attention to intermodal freight transport. A major cause of inefficiencies in rail freight transport is the location of intermodal terminals. Most terminals are located in the inner metropolitan areas and all freight transport has to enter and exit through these highly congested areas.

Road and rail services are often complimentary with investments in one mode having effects on the utilisation of the other. Reviewing and developing road, rail, urban congestion and land use policies in isolation is unlikely to solve problems issues facing the rail industry or the problems facing cities as they continue to grow.

The growth and geographic expansion of cities has brought formerly outer suburbs to terminals that were built outside the city area and many terminals are now being encircled by residential and commercial areas. Consequently, urban growth has reduced the productive potential of existing terminal assets.

The demand for non-bulk freight transport is forecast to grow faster than the rate of economic growth. However, the rail industry's ability to address this increased demand is constrained by the adequacy and location of corridors and freight facilities. Terminals are needed with optimal road and rail links, ability to handle long trains with minimal shunting, and scope for long-term capacity growth.

The rail industry has proposed strategies to address these issues that would see:

The promotion of the development of a network of intermodal terminals in outer

urban industrial centres with efficient rail and road links; and

Encouragement for container storage, packing and other value adding activities to be

progressively located at or near these outer-urban terminals, away from the central port precinct towards rail, and reduce urban road congestion costs caused by having a sub-optimal over-use of roads.

Future Developments

Freight handling methods continually evolve, seeking new and more efficient ways to move goods from point A to Point B. The key drivers of these developments include:

Economy of scale - larger parcels for handling can generally be more cost effective;

Advances in technology – containerisation, roll-on/roll-off methods, packaging of

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Increases in ship size – largely driven by the need for economies of scale;

Increased cost of labour – observed in all markets and in developed world in

Increased energy costs – likely to become increasing important post peak oil; and

Legislation and standards - particularly safety, emissions and materials handling.

These drivers have resulted in larger cargo handling equipment and changes to operating practices and the storage and transport of cargo. Increases in the cost of commodities and goods and increases in the cost of fuel have led to shippers and cargo handlers wanting to increase the average parcel size. This has also been driven by increases in ship sizes again in response to the need to make cost savings by economies of scale. Of particular note for the Central Queensland Intermodal Logistics Hub:

Cargo handling equipment in ports, storage areas and at manufacturers has changed

considerably and it is envisaged cargo handling equipment will continue to have increased lifting capacity, to be able to lift with greater reach and to lift at increased speeds (within limitations). Cargo handling equipment in the storage yard is also increasing in size and number due to the increase in parcel size.

Currently the majority of cargo handling equipment is powered by non-renewable

energy sources including diesel fuels and electricity from coal or gas fired power stations. In order to reduce green house gases equipment will need to be powered in future from renewable energy sources. Diesel powered equipment is slowly being converted with fuel saving hybrid systems but these are only a stop-gap solution as the equipment still emits carbon dioxide. The amount of legislation and regulations related to environmental improvement and reducing green house gases will increase and will affect the type of cargo handling equipment and cargo handling methods that are employed.

Hydrocarbon fuels will be phased out and more attention will be paid to reducing

noise levels of equipment both to protect operators and neighbours. Safety regulations will be tightened to further reduce injury and death with increasingly sophisticated control and sensing systems to reduce human error. The use of automated equipment will continue to rise as a way of eliminating man/machine interfaces and hence injuries.

Cargo handling equipment will increase in size and sophistication and more functions

will be automated. Prime movers will take energy from renewable sources and energy management will be included in all equipment. In 50 years time most mobile equipment and transport will be powered by fuel cells or hydrogen. Cargo parcels and units will continue to get larger and hence heavier.

Intermodal Facilities

The following table summarises the key characteristics of some examples of existing intermodal facilities in Australia.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Table 5.1. Characteristics of Selected Intermodal Facilities

Facility and Description

Brighton Transport Hub Tasmania

The Brighton Transport Hub is a $79 mil ion Intermodal Transport hub covering 50 hectares currently under

construction in conjunction with the Brighton Bypass on the northern fringes of Hobart. The Bridgewater

Industrial Estate was chosen as the preferred site of the Inland port because of its close proximity with the Midland Highway and the State's southern railway line.

On completion the facility facilitate the transfer of freight between road and rail transport and increase freight

efficiencies between Tasmania's southern and northern ports (The Department of Infrastructure, Energy and

Resources 2012). The Brighton Bypass is a critical part of the development wil provide improved connections to and support for the development of the new freight transport hub. The $79 mil ion hub is expected to be

operational by September 2011 and the $164 mil ion Bypass is scheduled for completion by June 2012.

This project aims to provide:

o A highway system to accommodate Tasmania's growing freight task, which is projected to double by 2022. o A highway system that supports the changed direction of trade from southern Tasmania to the northern

o A more consistent operating environment for freight traffic and passenger vehicles. o Reduced freight travel times and improved transport efficiencies for freight vehicles, travel ing between the

Southern Region and northern destinations.

o Reduced conflict between the through traffic function of the Highway and the local access requirements of

the Brighton area.

o Benefits to industrial and warehousing activities, supporting economic growth in southern Tasmania. o Seamless connections between road/rail freight via the Brighton Transport Hub. o Improved access to the developing Brighton Industrial Estate. o Safer road network for al users by addressing many safety issues associated with the deficiencies of the

existing highway.

o Reduced road trauma and the associated economic costs of crashes to the community o Significant social benefits through improved amenity in Brighton and Pontvil e.

The projects are considered fundamental to the long-term importance for the future of transport in the region

and wil provide a modern road-rail interchange and freight distribution hub to improve the efficiency of freight movement into and out of southern Tasmania.

Western Sydney Intermodal Hub

P&O Trans Australia and QRN operate a domestic and international rail hub at Yennora in western Sydney.

The hub includes an intermodal terminal which wil cater for QR's national intermodal business and also a new

port shuttle service carrying international cargo to and from Port Botany. The shuttle service has the capability

for 10 train services per day to and from Port Botany and domestic capital cities.

The Yennora hub provides industry with an all-rail service linking Port Botany to western Sydney via the port

shuttle and throughout Australia using a domestic rail service.

The port shuttle can handle container traffic to and from Port Botany by rail in larger volumes and more

reliably than is currently possible by road, given congestion levels.

A critical advantage of the Yennora development was the opportunity to allow customers access to a ful y

integrated rail transport solution with the ability to connect from vessel to rail to terminal to customer to national distribution.

The Yennora development includes rail-based warehousing at the site, allowing for the distribution of domestic

and international product throughout Australia from a single facility. The site also includes empty container

storage, repairs and handling facilities to remove unnecessary road legs from the transport chain and make international containers readily available to exporters. Other benefits include a central receival terminal for

container packing of domestic and international loads and the provision of a ful range of Customs and AQIS handling services, removing the need to deliver boxes to third party facilities for inspection and treatment.

There wil also be a transport fleet on site to provide on time pickup and delivery for customers in the area.

Acacia Ridge

Primarily used for interstate and intrastate rail freight movements.

Lack of capacity to accommodate some train lengths.

Some space limitations at precinct.

Links to surrounding road network north, south and west.

Hub is landlocked and prone to flooding.

Key industrial areas are in proximity to major roads that service the hub.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Facility and Description

Bomen Business Park Wagga Wagga

The Bomen Business Park aims to be a high-quality and nationally renowned place for transport and logistics-

based enterprises, wel -designed and integrated with existing industry, which meets the requirements of a targeted range of businesses and supporting activities; to complement and nurture a more sustainable City of

Wagga Wagga and Riverina Region.

Bomen Business Park straddles either side of railway between Melbourne & Sydney and also has excel ent

access to state and national road network. Close proximity to Wagga's airport.

More land area available and it is proposed to establish the Riverina Intermodal Freight and Logistics (RIFL)

Hub at the Bomen Business Park involving the construction of integrated rail, road and freight logistics

The RIFL Hub wil provide freight consolidation, logistics support and open access rail transport services for

businesses throughout the Riverina and wil include a grain packing service and container storage site

The Hub wil initially focus on providing bulky goods long line-haul rail services to and from the ports of

Melbourne, Sydney, Port Kembla and Brisbane.

Parkes sits on Newel Highway, the major freight route between Melbourne & Brisbane (1400 heavy vehicles

Road train access from Adelaide as wel .

Planning to develop strategic road transport plan, that meets access needs of Parkes hub while also protecting

the local residential amenity.

Linked by rail to Sydney, Perth, Melbourne, Brisbane, Adelaide.

Steep topography and curfew in metro areas provide constraints.

Hub provides rail access to numerous ports.

Main industries of town are copper & gold mining, wheat, wool, transport & storage.

Central Queensland Intermodal Logistics Hub

Central Queensland is traversed by the main north south rail line between Brisbane and Cairns and includes the current intermodal facilities in the centre of Rockhampton and at Port Curtis. Freight trains heading north from Brisbane and south from Cairns and Townsville collect and drop off wagons on their onward journey which are then transported to their final destination throughout the region using road haulage.

While the worldwide growth in containerisation has been reflected in the region, many of the major commodities which move through the region are unsuited to being transported in this way including:

Coal and other bulk commodities – coal and other bulk commodities are moved

through and around the region in specialist vehicles (road or rail) with no benefit, and potentially significant additional costs, from transhipment at an intermodal facility.

Mining equipment – the high value of some mining parts and equipment and more

importantly the opportunity costs of lost time waiting for parts means that many pieces of equipment are moved between suppliers and the consumers on a courier type basis. There is very limited opportunity to move these types of equipment by intermodal transport.

Fuel – fuel is landed at Port Alma and the Port of Gladstone and then distributed by

road based transport. While historically many smaller settlements maintained their own fuel bunkering facility, additional environmental controls and improvements to vehicles and the road network mean these operations are no longer viable. There is no benefit from collecting fuel supplies at the quayside and moving them by rail to a separate storage facility from which final distribution is made by road. Instead, fuel is loaded from large storage tanks at the port and driven straight to the final consumer or retailer.

Cattle – the Central Queensland region is renowned for its beef production but very

little now moves by rail. Increased competition for space on some networks and the additional flexibility offered by road based haulage has significantly reduced the volumes of cattle and beef products moved by rail. Discussion with industry suggests this is very unlikely to change in the foreseeable future.

Grains – as with cattle, grain transport has shifted away from rail as a result of

competition for space with bulk commodities. While some storage and consolidation is

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

required, this is undertaken in the primary grain growing areas before transport to domestic markets or for export.

Horticultural production – the absolute volume of horticultural production in the

region is too small and too seasonal to support an intermodal facility. Goods would need to be loaded at the farm gate, brought to the intermodal hub put onto a train then unloaded and driven to the wholesale markets or processors. This double handling would be uncompetitive compared to road only transport.

It is not as simple as identifying total freight demand in the region and deciding that this alone can justify an intermodal facility. However, two such facilities exist in Rockhampton. Discussions with the operators suggest both facilities are viable although constrained in terms of future growth at their current location. The principle goods which are moved through the facility include:

Food – much of the food supplies for Central Queensland are brought into the region

by rail for onward distribution into stores by road. This supply line is in addition to supplies which are brought in by road straight from supermarket distribution centres and smaller producers.

Retail Supplies – supplies for other retailers, other than food, are also brought in by

rail and again are then distributed around the region by road.

General Cargo – some consolidated loads are also brought into the region by rail for

sorting/destuffing/consolidation and onward distribution by road.

Construction Costs

Preliminary discussions with stakeholders suggests the estimated capital investment needed to establish the intermodal equipment needed, excluding all other development costs is estimated to be between $35-$40 million. Unlike the development of a logistics hub, or other warehousing and industrial development, there could be very limited opportunity for staging the development to match any ramp up in demand over time. The facility would need to be established at its final scale with future expansion through duplication of the equipment on the ground.

For these types of facility to be successful, it would need to be operating on a continuous 24 hour basis all year round. While some seasonality could be accommodated, the operating model would need to be centred around a few key high volume products which would account for the majority of throughput with additional seasonal demand a bonus.

Barriers to Entry

Given the apparent success of the existing facilities it might appear logical that they should be relocate to a new site in the region where the current constraints and conflict of use issues are removed. However, this fails to recognise the investment both organisations have made in their existing infrastructure. Although constrained these issues are not so severe that they would consider moving without some form of compensation. Stakeholders recognise the value in the move but from a practical point of view understandably are unwilling to walk away from their investment.

The Future

The freight industry has changed significantly in the last twenty years and the intermodal sector in particular. The advent of satellite tracking systems, optimisation software and the move towards automated just in time inventory management systems have all had major impacts on the logistics sector. It is unlikely the pace of this change will slow down and indeed might increase. Future changes are likely to impact upon the feasibility of an intermodal facility, including:

Carbon price – The Carbon Price Mechanism places an impost on every tonne of

Green House Gas emissions produced by large emitters from 1 July 2012. For the first three years, the carbon price will be fixed. It will then transfer to an emissions trading scheme on 1 July 2015. While transport related emissions are currently largely exempt, it is almost certain that in the medium to long-term a market based carbon price will be applied to the transport sector. While these prices are likely to be passed on the end consumer, the relative carbon contribution of different transport

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

modes is likely to have a significant impact on the volume (and value) of freight moved. It is likely that rail and sea freight (containerised and bulk) will become more competitive with road freight over shorter distances.

Planning and development - An investment of the magnitude needed to establish

an intermodal facility is almost certain to be a long-term consideration with operating profits needed to provide an appropriate return on investment over the long-term. In considering investment of this nature one of the key considerations is the major infrastructure developments likely of take place in the payback period and the impact of these developments on the feasibility of the investment.

There is limited opportunity to establish a viable intermodal logistics hub in the Central Queensland catchment. There are existing facilities operating in the region and many of the goods which are required as a result of the expansion of the resources sector are not suitable for intermodal transport. If it were possible to relocate the existing facilities out of Rockhampton to a new purpose built facility, it is likely this new consolidated facility would be viable. However, given the capital investment in the existing facilities there is strong resistance to moving unless appropriate compensation was available.

The impact of carbon pricing and peak oil on the price point at which rail becomes a more cost effective transportation option than road is unknown although it is widely agreed these macro factors will improve the competitiveness of rail. It is important the logistics hub is capable of incorporating a rail component over the long-term but in the short-term this should not be considered further in this assessment.

A road based logistics precinct, which seeks to service identified demand for warehousing, secure storage and other industrial sites as well as accommodating a series of ancillary industries may offer a more realistically viable opportunity.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

6. Demand for a Logistics Hub

Key Findings and Implications:

There are large and growing freight flows through the Central Queensland.

The majority of these flows are South-West and North-South.

The majority of these flows (excluding bulk commodities) are undertaken by road.

There may be an opportunity to establish a facility which meets the needs of the

transport sector as well as pursuing other related opportunities which have been identified.

There is widespread support for the concept of a logistics hub and stakeholder

recognise the potential advantages of a purpose built and well located facility as well as the opportunities to benefit from locating nearby customers and suppliers.

Some existing operators are reticent to move from the existing locations where they

have made significant investment in capital improvements.

Potentially Viable Oppportunities

The following table summarises stakeholder comments on potential freight flows through a logistics hub in the region and the ancillary suppliers likely to be attracted to of such a facility.

Pre-Feasibility of a Central Queensland Intermodal Freight Hub Final Report

Figure 6.1. Potentially Viable Opportunities at a Logistics Hub

Opportunity

Benefits from Location in CQ

Benefits to Other Users

Future Prospects

Mining Services Parts Storage and Distribution

The opportunity costs of mining CQ is wel positioned to service Mining support services could

Existing operators are unlikely

There is a strong expectation of

operations being held up while

three major resource provinces

act as a potential anchor for the

to abandon current sites but

sustained increased mining

waiting for parts can run into

(Surat, Bowen and Galilee)

future growth is constrained

activity in the region and

mil ions of dol ars